What if your medical history was viewed as a roadmap for proactive care rather than a reason for rejection? It’s a common frustration to feel that a previous diagnosis permanently locks you out of private support, particularly when the NHS waiting list remains at a staggering 7.6 million people. You’ve likely felt the sting of “small print” exclusions or the fear that your history makes you uninsurable. Finding effective health plans for pre existing conditions shouldn’t be an uphill struggle against rigid corporate rules that ignore your individual needs.

We understand the exhaustion of being told “no” because of a condition you’ve managed for years. This guide shows you exactly how to secure comprehensive support in 2026, including immediate 24/7 GP access and mental health care that acknowledges your journey without dismissing it. We’ll demystify the complexities of moratorium and full medical underwriting to provide you with total clarity. We explore how a 360-degree approach to wellness can turn a complex medical history into a manageable, supported path toward long-term resilience.

Key Takeaways

- Demystify how UK insurers define medical history and what it means for your ability to secure comprehensive private cover in 2026.

- Navigate the complexities of Full Medical Underwriting versus Moratoriums to choose the most protective assessment method for your unique circumstances.

- Uncover why traditional insurance often fails for long-term care and how to avoid the common pitfalls of the “chronic condition trap.”

- Explore innovative health plans for pre existing conditions that utilise subscription models and Medical History Disregard to offer inclusive, proactive support.

- Discover how to access a 360-degree view of your health with 24/7 Virtual GP services that provide expert clinical guidance without medical exclusions.

What are pre-existing conditions in the UK health market?

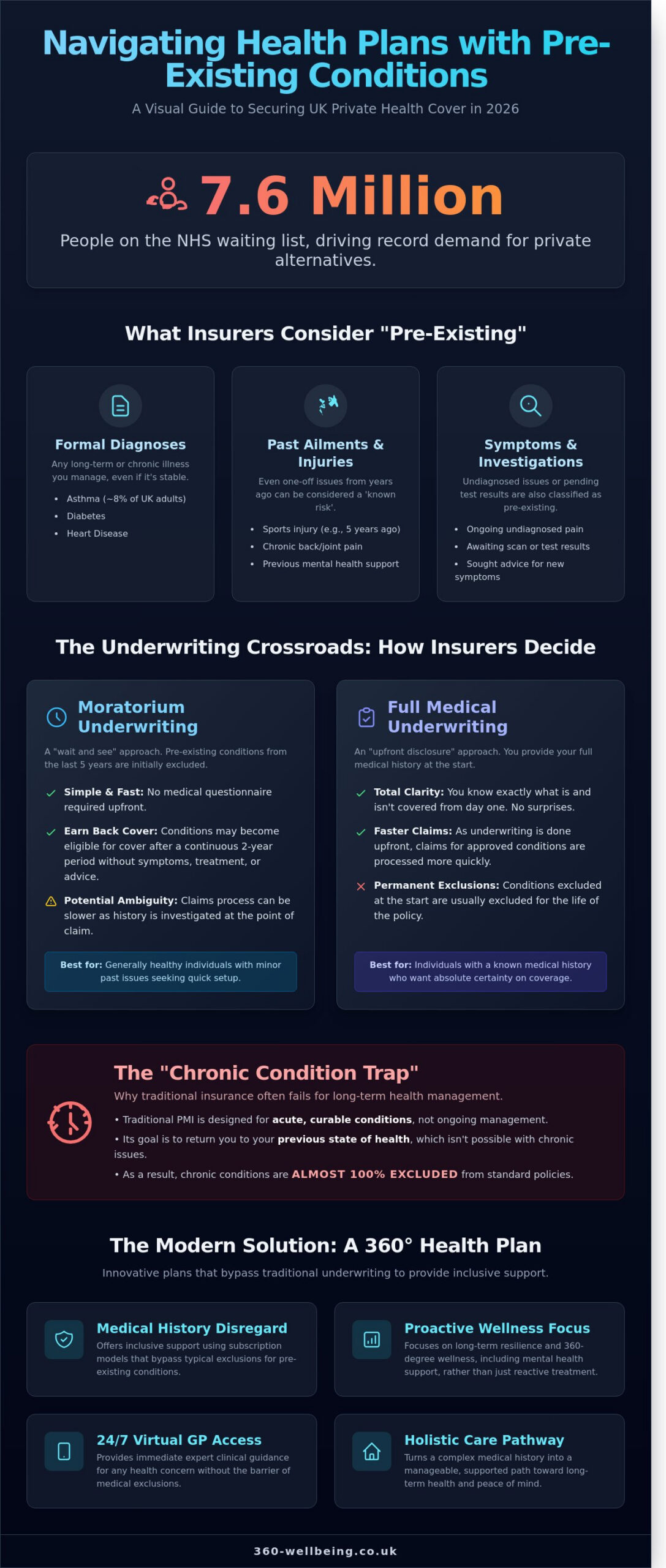

When you begin looking for a new private medical policy, the insurer will look closely at your medical history. This process is essential for providing a clear, transparent agreement between you and the provider. Fundamentally, What are pre-existing conditions refers to any ailment, illness, or injury you’ve experienced before your cover begins. This isn’t limited to long-term illnesses; it spans a broad spectrum from a one-off sports injury five years ago to a chronic lifestyle condition you manage daily.

Insurers view these history markers as ‘known risks.’ While insurance is designed to protect against the unexpected, a condition that’s already present represents a predictable requirement for care. This distinction is why most standard private policies exclude these conditions through a process called underwriting. However, the market is evolving. Many providers now offer specialised health plans for pre existing conditions that use moratorium underwriting or specific corporate schemes to offer a path toward cover after a set period of being symptom-free.

It’s vital to understand that a ‘condition’ isn’t just a formal diagnosis written in your GP records. UK insurers also consider symptoms and pending investigations. If you’re currently waiting for test results or have been experiencing undiagnosed joint pain, these are classified as pre-existing. Transparency at the application stage builds a foundation of trust. It ensures that when you do need to make a claim, the process is smooth and the support is immediate.

Common examples of pre-existing conditions

In the UK, certain health trends frequently appear on medical applications. Chronic respiratory issues like asthma affect roughly 8% of the adult population. While manageable, insurers track these to understand potential secondary complications. Musculoskeletal problems are equally common; chronic back pain and joint issues often require ongoing physiotherapy or specialist consultations. Mental health is another significant area. If you’ve had previous bouts of anxiety or depression, insurers look at the 360-degree view of your wellbeing history to determine how best to support your future mental resilience.

The 2026 NHS context and private health demand

The relationship between private health and the NHS is shifting as we approach 2026. With NHS waiting lists sitting at approximately 7.6 million people as of early 2024, the demand for private alternatives has reached a record high. People are no longer just looking for emergency cover; they’re seeking health plans for pre existing conditions to manage long-term wellness without the stress of extended wait times.

By 2026, the focus on secondary care in the private sector will likely intensify. This involves managing chronic conditions through private specialists rather than relying solely on the state. We’ve already seen a 25% increase in ‘pay-as-you-go’ healthcare since 2022. This model allows individuals to fund specific treatments for pre-existing issues while keeping a traditional insurance plan for new, unforeseen illnesses. This hybrid approach ensures you remain proactive about your vitality, regardless of your medical history. It’s a strategic way to maintain workplace harmony and personal peace of mind in a changing healthcare environment.

How traditional health insurance assesses your medical history

Traditional Private Medical Insurance (PMI) operates on a risk-based model known as underwriting. This process acts as a gatekeeper; it determines which ailments the insurer will cover and which they will exclude based on your past health. Most standard PMI policies are designed to treat acute, curable conditions rather than long-term management. This is a crucial distinction for anyone seeking health plans for pre existing conditions, as the approach to your history dictates your future coverage levels.

Insurers generally view any condition you have suffered from in the past five years as a higher risk. When they assess your history, they often refer to specific clinical lists to categorise your health. You can find more detail on what are pre-existing conditions through official NHS guidelines, which highlight chronic issues like heart disease or type 2 diabetes that typically fall outside standard coverage. Because standard PMI aims to return you to the state of health you enjoyed before an acute episode, chronic conditions are almost 100% excluded. In fact, industry data suggests that 95% of individual PMI policies in the UK will not cover the routine management of long-term illnesses.

Understanding Moratorium Underwriting

Moratorium underwriting is the most common choice for individuals because it doesn’t require a medical exam at the point of application. Instead, the insurer applies a blanket rule to your history. A moratorium policy automatically excludes any medical condition you’ve experienced in the five years prior to your policy start date. This is a rolling period, meaning it rewards periods of sustained health.

The ‘two-year trouble-free’ rule is the cornerstone of this method. If you join a plan and go two consecutive years without seeking treatment, taking medication, or even receiving professional advice for a past condition, that condition may eventually be covered. However, even a single prescription or a quick chat with a GP during those 24 months resets the clock. It’s a strict threshold that requires total transparency and patience from the policyholder.

The Full Medical Underwriting (FMU) process

Full Medical Underwriting (FMU) takes a more proactive and detailed approach. You’ll complete a comprehensive health questionnaire detailing your entire medical history. While this feels more intrusive, it offers the advantage of certainty. You’ll know exactly what’s covered from day one because the insurer lists every specific exclusion on your membership certificate. There’s no ambiguity when it comes to making a claim later.

During this process, an insurer might request a formal report from your NHS GP to clarify specific points in your history. This happens in roughly 15% of FMU applications. If the insurer decides to cover a slightly higher-risk condition rather than excluding it entirely, they might apply ‘premium loading’. This can result in a price increase of 10% to 30% above the standard rate. For those specifically looking for health plans for pre existing conditions, FMU provides a clearer roadmap, even if it comes with higher initial costs or specific caveats. It replaces the ‘wait and see’ nature of a moratorium with a defined, albeit sometimes limited, contract of care.

The Chronic Condition trap: Why insurance often fails

Most people discover the limitations of Private Medical Insurance (PMI) at their most vulnerable moment. Traditional PMI operates on a “fix and discharge” model. It’s designed to step in when you have a specific, curable problem and step out once you’re stable. For the 15 million people in England living with long-term health issues, this creates a significant gap in care. When a condition requires ongoing management rather than a one-off surgery, insurers often label it as chronic and cease funding.

The emotional toll of being told a condition is uninsurable shouldn’t be underestimated. It feels like a rejection of your personal history. When an underwriter places a blanket exclusion on your policy, they aren’t just saying they won’t pay for a specific pill. They’re often excluding entire body systems. A single recorded instance of lower back pain three years ago can result in a total exclusion for any spinal issues, leaving you to rely solely on NHS waitlists that currently exceed 7.6 million people for elective treatments.

Acute vs Chronic: The clinical dividing line

Insurers distinguish between acute flare-ups and chronic maintenance. An acute episode is a brief, severe event like a gallbladder removal or a sudden hernia. PMI excels here. However, conditions like Type 2 diabetes or high blood pressure are categorised as maintenance-only. You’re expected to pay for your own blood monitoring and routine prescriptions. By 2026, the UK healthcare sector expects a major shift toward holistic management, yet many traditional insurers still refuse to cover the lifestyle coaching or nutritional support that prevents these conditions from worsening. This rigid definition often leaves patients feeling abandoned by the very policies they bought for peace of mind.

Addressing the #1 objection: ‘I’m paying for nothing’

It’s a common frustration. You pay £1,200 a year for a premium policy, yet your primary health concern is excluded because it’s pre-existing. It’s easy to feel like you’re throwing money away. However, the value of insurance often lies in the “what ifs” rather than the “what is.” Even if you have exclusions, modern plans provide vital access to diagnostic hubs and cancer cover. With 1 in 2 people in the UK born after 1960 expected to be diagnosed with cancer in their lifetime, having a fast track to oncology is a powerful safety net.

Smart consumers are now looking for a 360-degree approach. They realise that standard PMI isn’t a silver bullet. Instead of relying on a single policy, a hybrid strategy is becoming the UK standard. This involves using virtual GP services for daily needs while keeping PMI for catastrophic events. When searching for health plans for pre existing conditions, it’s vital to look for services that offer proactive wellbeing support rather than just reactive hospital cover. A proactive plan helps you build resilience, ensuring that even if your condition is excluded from surgery, you still have the tools to manage your vitality daily. Relying on a balanced mix of support ensures you aren’t left waiting in a system that’s increasingly stretched thin.

Evaluating alternatives: Health plans vs. Health insurance

Traditional Private Medical Insurance (PMI) often functions as a reactive safety net. You pay a premium and wait for a significant health event to trigger a claim. Subscription-based health support platforms offer a different path. These models focus on proactive, daily wellness rather than just crisis management. They create a continuous ecosystem of care that supports you before a small concern becomes a chronic issue.

Choosing between these options usually depends on your specific needs for long-term security versus immediate, everyday access. While PMI is designed to cover the costs of private hospital stays and surgeries, health support platforms provide the tools for ongoing vitality. For many UK businesses, the predictability of a subscription fee is more manageable than the fluctuating costs of insurance premiums, which rose by an average of 12% in 2023 due to medical inflation.

What is Medical History Disregard?

Medical History Disregard (MHD) represents the highest tier of corporate health cover. It allows businesses to provide medical insurance that ignores the past health issues of their staff. This is a vital tool when seeking health plans for pre existing conditions, as it ensures everyone is covered from their first day of employment. In the UK market, most providers require a minimum group size of 15 to 20 employees to offer MHD terms. It removes the stress of individual medical declarations, making it an inclusive, compassionate choice for a diverse workforce.

The rise of Virtual GP and Mental Health platforms

Digital health platforms have transformed how we access primary care. Unlike traditional insurance, these platforms don’t require complex underwriting because they focus on primary support and preventative health. You don’t have to prove you’re already healthy to get help. This makes them highly effective health plans for pre existing conditions that require regular check-ins or prescription management.

The speed of access is the most significant benefit. While the average wait for an NHS GP appointment can now exceed 10 days in many regions, virtual platforms offer 24/7 access. You can often speak to a doctor within minutes. This immediacy prevents minor symptoms from escalating. These platforms also offer a 360-degree approach to wellness by integrating various services into one app:

- 24/7 Virtual GP: Immediate consultations for prescriptions, referrals, and advice.

- Integrated Mental Health: Direct access to counselling and CBT without waiting for a specialist referral.

- Holistic Physical Care: In-app physiotherapy assessments and tailored exercise programmes.

- Life Coaching: Proactive support for stress management and nutritional guidance.

Comparing the financial commitment is also essential. A comprehensive PMI policy for a single employee can cost upwards of £600 per year, and that price often increases as the individual ages. Health support platforms typically operate on a flat subscription fee, often between £5 and £15 per month per person. This makes high-quality care accessible to a much broader range of people, ensuring that support is a fundamental right rather than a luxury.

Ready to provide your team with inclusive, proactive care that covers everyone? Explore our tailored corporate health plans to see how we can support your business goals.

Securing your health with 360 Wellbeing

Achieving true vitality requires more than just a reactive approach to illness; it demands a 360-degree view of your physical, mental, and social health. At 360 Wellbeing, we provide a unified platform that treats these elements as interconnected parts of a whole. Our 24/7 Virtual GP service offers immediate access to UK-registered doctors who can provide advice, prescriptions, and referrals without the typical barriers found in traditional insurance. Unlike many private providers that place strict limitations on chronic issues, our service is designed to be inclusive. We provide a reliable safety net for those seeking health plans for pre existing conditions, ensuring that your medical history never prevents you from receiving high-quality care.

Our support system extends far beyond a standard consultation. We offer comprehensive mental health services and physiotherapy to all members, addressing the two primary causes of workplace absence in the UK. According to 2023 HSE data, 32.5 million working days were lost due to work-related ill health, with stress, depression, and musculoskeletal disorders accounting for the majority. We tackle these challenges head-on by providing direct access to specialists. This proactive model helps you manage symptoms before they escalate, fostering long-term resilience and health stability for every member of our community.

The platform serves as a logical choice for individuals who find themselves priced out of traditional private medical insurance. Because we operate as a wellbeing support service rather than a standard indemnity product, we can offer consistent, high-level care to everyone. This makes us a primary destination for those searching for health plans for pre existing conditions that offer immediate value without the wait. Our focus remains on your future health potential rather than your past medical records.

- 24/7 Virtual GP: Speak to a UK doctor anytime, anywhere, with no medical exclusions for consultations.

- Mental Health Support: Access to qualified counsellors to build emotional resilience and manage stress.

- Physiotherapy: Expert guidance to recover from injuries and improve physical mobility.

- Holistic Care: A unified approach that connects all aspects of your wellbeing in one app.

Inclusive care for everyone

We believe that health support should be accessible to all, which is why we don’t ask for a medical exam or a complex health questionnaire to join our platform. This open-door policy is particularly beneficial for employees with chronic conditions who often feel overlooked. We provide tailored life coaching to help these individuals manage their daily wellness and maintain workplace harmony. To make this support even more sustainable, our 360 Rewards programme offers discounts at major retailers, potentially saving members over £1,200 a year, which effectively offsets the cost of their wellbeing subscription.

Getting started: A proactive path to vitality

Setting up a plan is a straightforward process designed for speed and clarity. Small business owners can organise coverage for their entire team in a single afternoon, providing a strategic asset that boosts morale and reduces absenteeism. Sole traders and individuals benefit from the same simple onboarding, gaining instant access to our suite of clinical and lifestyle tools. You can take the first step toward a more balanced life today. Discover how 360 Wellbeing supports your medical history and provides the comprehensive care you deserve.

Empower Your Team With Inclusive Care Today

Navigating the UK’s private healthcare landscape in 2026 shouldn’t feel like a series of closed doors. We’ve explored how traditional medical underwriting often leaves those with chronic histories behind; this creates a gap in care that impacts long-term employee resilience. By prioritising health plans for pre existing conditions, you ensure every team member receives support without the stress of complex medical assessments. Our platform removes these barriers, offering a proactive 360-degree approach that values every individual’s health journey.

You can secure your team’s health with our inclusive 360 Wellbeing platform to provide immediate, reliable support. Your staff will benefit from 24/7 access to UK-registered Virtual GPs, while mental health and physiotherapy services are included as standard to support the 1 in 4 UK adults who experience mental health challenges each year. Because we require no medical underwriting for platform access, your entire workforce is protected from day one. It’s a straightforward path to building a healthier, more harmonious workplace where everyone feels seen and supported. We’re ready to help you take that next positive step toward total wellness.

Frequently Asked Questions

Can I get health insurance if I have already been diagnosed with cancer?

Yes, you can still purchase a policy, though the insurer will almost certainly exclude any treatment related to your existing cancer diagnosis. Most UK providers use moratorium underwriting, which excludes any condition you’ve had symptoms or treatment for in the last five years. Since one in two people in the UK will develop cancer in their lifetime according to Cancer Research UK, insurers are very specific about these exclusions to manage risk.

What is the difference between a health plan and health insurance?

A health plan typically provides fixed cash payments towards routine healthcare costs, while health insurance covers the actual cost of private hospital treatment for acute conditions. Many people choose 360 Wellbeing health plans for pre existing conditions because they offer immediate access to Virtual GPs and mental health support without the lengthy exclusions found in private medical insurance. While insurance premiums averaged £1,155 in 2023, cash plans remain a more affordable entry point for daily care.

Do I have to declare my medical history when joining 360 Wellbeing?

No, you don’t need to undergo a medical exam or provide a full history to access our primary care services. We believe in proactive health management, so our Virtual GP and wellbeing tools are available to you from day one. This approach removes the barriers often found in traditional insurance, allowing you to focus on resilience and recovery rather than paperwork and past diagnoses.

How long does a moratorium period usually last in the UK?

A moratorium period typically lasts for two years of continuous cover. If you don’t seek medical advice, take medication, or experience symptoms for a pre-existing condition during those 24 months, the insurer may begin covering that condition. It’s a standard industry timeframe designed to ensure a condition is truly in remission before the provider takes on the financial risk of private treatment.

Can my employer provide a health plan that covers my pre-existing condition?

Yes, many employers offer “Medical History Disregarded” (MHD) schemes which are excellent health plans for pre existing conditions. These group policies are usually available to businesses with 15 or more staff members and allow employees to claim for past illnesses immediately. It’s a powerful way for companies to support workplace harmony, as it ensures every team member receives the same high level of clinical care regardless of their health history.

Will my premium go up if I develop a new condition after joining?

Your premium won’t increase immediately upon a new diagnosis, but you will likely see a rise at your annual renewal date. In 2023, UK medical inflation and age-related adjustments caused premiums to rise by an average of 7 percent across the industry. While your individual claims history can influence the price, insurers also spread the cost across their entire pool of policyholders to keep individual increases manageable.

Is mental health support included for people with a history of depression?

Yes, our wellbeing services provide immediate access to mental health professionals regardless of your clinical history. We offer structured counselling sessions and 24/7 helpline support to help you maintain a 360-degree perspective on your wellness. Unlike traditional insurance that might exclude “chronic” mental health issues, we view psychological support as a fundamental right that should be accessible the moment you feel the need for guidance.

What happens if I forget to disclose a condition on an insurance application?

Your insurer may refuse to pay a claim or even cancel your policy entirely if they discover an undisclosed condition. Under the Consumer Insurance (Disclosure and Representations) Act 2012, you’re required to provide honest and accurate information to the best of your knowledge. If a non-disclosure is found during a claim for a £5,000 surgery, the financial consequences for you could be life-changing, so it’s vital to be thorough during the application.